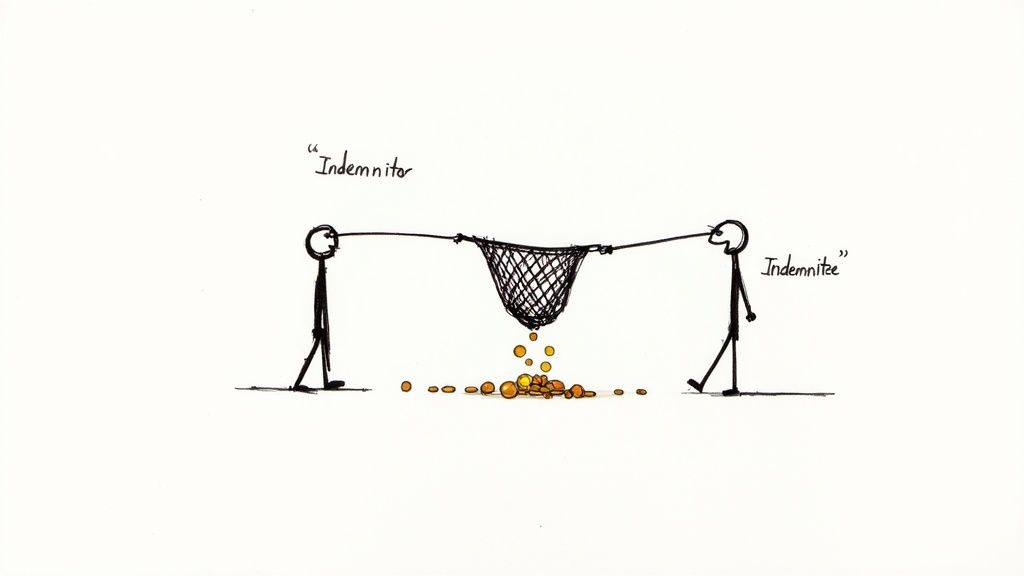

An indemnification clause is a promise in a contract where one person agrees to cover the costs for another if something specific goes wrong.

Think of it as a financial safety net you set up in advance. It’s designed to answer one key question before any problems pop up: "Who pays if there's a mess?"

Understanding the Basics of Indemnification

Let’s use a simple example. Imagine you hire a contractor to remodel your kitchen. The contract you sign has a clause saying the contractor will pay for any damage they cause to your neighbor's property while working.

That’s an indemnification clause. It moves the financial risk for that specific problem from you to the contractor.

This setup involves two key players, and it's important to know who's who.

Who's Who in an Indemnification Clause

To keep things straight, here's a quick table to help you understand the roles at a glance.

| Term | Simple Explanation | Example Role |

|---|---|---|

| The Indemnitor | The one making the promise to pay. | The kitchen contractor |

| The Indemnitee | The one getting the promise and protection. | You, the homeowner |

By defining these roles before any work starts, the clause creates a clear plan for handling potential screw-ups. This simple step can save everyone from major headaches and expensive fights down the road.

Why This Clause Is So Common

You'll run into these clauses everywhere—from your apartment lease and freelance agreements to the terms of service for your favorite app. Their main job is to manage and assign risk.

Without them, figuring out who should pay for a loss can turn into a messy, time-consuming legal battle. And nobody wants that.

They are especially common in business deals. In fact, a study of 811 vendor contracts found that a whopping 85% required the customer to cover the vendor for certain issues. This shows just how often businesses use these clauses to shift potential costs to others.

An indemnification clause doesn’t stop mistakes from happening. It just provides a clear roadmap for who is financially responsible when they do, giving everyone a bit of predictability and peace of mind.

Understanding this core idea is the first step to making sense of otherwise scary-looking legal documents. While the language can be dense, it almost always boils down to this simple transfer of risk.

If you're looking to get more comfortable with legal documents, our guide on understanding common legal terms in English is a great place to start.

Why Indemnification Clauses Appear in So Many Contracts

Ever wonder why this clause seems to pop up everywhere? The reason is simple: risk management. Every single agreement, whether you're hiring a freelance designer or signing up for a new software service, comes with some level of risk. This clause is just a pre-agreed plan for who pays the bills if something goes wrong.

Let’s make this real. Imagine you hire a contractor to renovate your office. During the job, they accidentally drill through a wall and burst a water pipe, flooding the business next door. Without an indemnification clause, you could get dragged into a messy legal fight with your neighbor, facing a mountain of legal fees and damages—even though it wasn't your fault.

A solid indemnification clause flips that script. It says upfront that the contractor (the indemnitor) is on the hook for those costs, protecting you (the indemnitee) from the financial fallout.

Creating Predictability and Peace of Mind

At the end of the day, this clause brings a much-needed dose of predictability to business deals. It lets both sides know exactly where they stand financially if a specific problem arises. That kind of clarity is what builds trust and lets projects move forward.

Here’s why these clauses are so common:

- Protecting the Innocent Party: It’s designed to make sure the person who didn’t cause the problem isn't left holding the bag.

- Avoiding Costly Disputes: By setting the rules in advance, it helps prevent long, drawn-out court battles over who’s to blame.

- Encouraging Careful Work: When service providers know they are financially responsible for their mistakes, they tend to be a lot more careful.

Ultimately, an indemnification clause is about drawing clear lines around financial responsibility. It lets people and companies work together with more security, knowing they’re protected if something goes sideways because of the other party's actions.

Without understanding what an indemnification clause is meant to do, you're essentially walking into an agreement with a huge, undefined financial risk hanging over your head. It’s a foundational piece of modern contracting that makes complex partnerships and projects even possible.

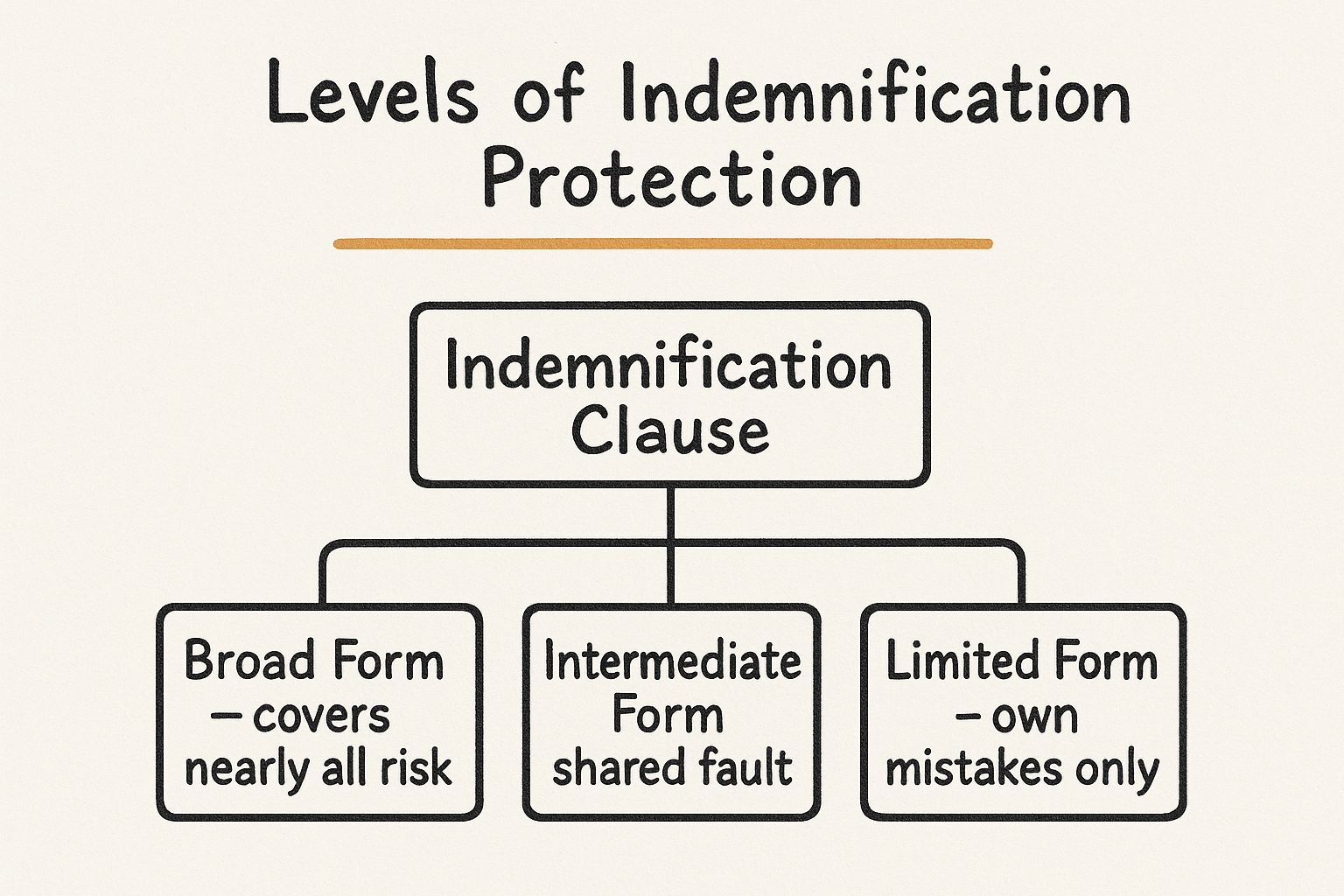

Understanding the Different Levels of Protection

Not all promises to pay are created equal. Just like car insurance policies offer different levels of coverage, these clauses come in several flavors, each shifting the risk in a different way. Getting a handle on these variations is the key to knowing exactly what you're signing up for.

Think of it like figuring out who pays after a fender bender. The outcome depends entirely on what the drivers agreed to beforehand. Some agreements pin almost all the responsibility on one person, while others split it more fairly.

This infographic breaks down the hierarchy of indemnification, showing how the levels of protection change from one type to the next.

As you can see, the clauses range from being extremely one-sided to much more balanced, which directly impacts your potential financial risk down the road.

The Three Common Clause Types

To make sense of what you might find in a contract, let’s unpack the three most common forms of an indemnification clause. Each one assigns responsibility in a unique way.

- Broad Form: This is the most one-sided version you'll see. The person promising to pay agrees to cover nearly all losses, even if the other party is partially or entirely at fault. It’s like being forced to pay for a car accident you didn't even cause.

- Intermediate Form: This type is a middle ground. The person promising to pay covers losses from their own actions and also any losses from shared fault. However, they are not on the hook if the other party is 100% to blame.

- Limited Form: This is the fairest and most common type in well-negotiated agreements. Here, each person is only responsible for the damages that come from their own negligence or mistakes. If both are at fault, they each pay their share.

This table gives a quick snapshot of how these clauses work in practice, clarifying who typically foots the bill.

Comparing Indemnification Clause Types

| Clause Type | Who Pays for Damages | Common Use Case |

|---|---|---|

| Broad Form | The one promising to pay covers all losses, regardless of fault. | High-risk contracts like construction, where one party holds most of the control. |

| Intermediate Form | The one promising to pay covers losses, unless the other party is entirely at fault. | Service agreements where fault might be shared but one party's actions are primary. |

| Limited Form | Each party pays for the damages they directly caused. | Partnership agreements and most balanced business contracts where risk is shared. |

Ultimately, recognizing the difference between broad, intermediate, and limited form clauses helps you accurately size up the level of risk you’re being asked to take on.

The most important takeaway? These terms are almost always negotiable. Identifying which type of clause is in your contract gives you the power to push for a fairer, more balanced agreement that actually protects your interests.

Real-World Examples of Indemnification Clauses

Okay, enough with the theory. Let's talk about where these clauses hide in plain sight. You’ve probably agreed to dozens of them without a second thought. They’re a standard part of all sorts of contracts, from service agreements to the terms you tap "Agree" to online.

Seeing what an indemnification clause looks like in the real world is the best way to really get it. When you translate the legalese into real stories, you start to see the promises you’re making and the risks you’re taking on.

Common Scenarios You Might Encounter

Here are a few everyday examples that show indemnification in action. Pay attention to who is protecting whom—and from what.

Rental Agreements: Your apartment lease almost certainly has one. It probably says that you (the indemnitor) will cover any damages or legal claims your landlord faces because of something your guest did. So, if a friend slips and gets hurt in your apartment, this clause shifts the legal headache from the landlord (the indemnitee) to you.

Freelance Contracts: A freelance graphic designer signs a contract promising to cover their client for any copyright infringement claims. If the designer grabs a stock photo without the right license and the client gets sued, the designer is on the hook for the legal bills—not the client.

Social Media Apps: When you sign up for a social media account, you agree to indemnify the company. If you post something that violates someone else’s copyright, this clause makes sure you’re the one who pays for any legal fallout, not the platform.

See the pattern? The core idea is always the same: one person agrees to step in and handle the financial hit if their actions cause a specific type of problem for the other person.

These clauses are also a non-negotiable part of high-stakes business deals. In asset purchase transactions, for example, they are absolutely crucial for deciding who is responsible for what. A market analysis of 154 such deals found that indemnification clauses were present in 95% of seller contracts and 89% of buyer contracts. That tells you just how vital they are. You can read more about these findings in asset purchase agreements on lexisnexis.com.

If you want a closer look at how these clauses get woven into online agreements, our guide on how to create a terms and conditions template is a great place to start.

How to Spot Red Flags and Negotiate Fairer Terms

Signing a contract with a one-sided indemnification clause can leave you in a tough spot. But here’s the good news: you don't need a law degree to spot the danger signs. Knowing what to look for and how to push back can help you secure a much fairer agreement.

The first step is to watch for overly broad or vague language. If a clause uses sweeping phrases that seem to cover everything, it’s time to hit the pause button.

Common Warning Signs in an Indemnification Clause

Pay very close attention to the wording. Certain phrases are specifically designed to shift an enormous, and often unfair, amount of risk onto your shoulders. Being able to spot them is the first step toward protecting yourself.

- "Any and all claims": This phrase is a massive red flag. It’s incredibly broad and could make you responsible for claims that are completely unexpected or have little to do with your direct actions.

- One-sided protection: A fair clause should be a two-way street. If the agreement only requires you to protect the other party, it creates an unbalanced situation where only their interests are shielded.

- Covering their negligence: This is the big one. The most unfair clauses will ask you to pay for the other party’s own mistakes. You should never have to cover losses that were caused by their negligence or misconduct.

Remember, your goal isn't to get rid of the clause entirely, but to make it fair. A balanced clause clearly defines responsibilities, ensuring each person is only on the hook for the mistakes they actually make.

It's also worth noting that market conditions can influence these terms. For example, research on R&D contracts shows that indemnification clauses become more common when market competition heats up, as companies scramble to manage the heightened risks of aggressive innovation. You can find more insights on how competition affects contract terms on nottingham-repository.worktribe.com.

Simple Tips for Negotiating a Better Deal

Once you spot a red flag, it’s time to negotiate. Your aim is to make the terms more specific, limited, and balanced.

Start by asking for a mutual indemnification clause, where both sides agree to protect each other from their respective mistakes.

You can also propose adding a simple "to the extent" phrase. This addition is powerful because it limits your responsibility to only those losses directly caused by your actions.

And if you're feeling overwhelmed, our guide on how to read contracts effectively can give you the extra confidence you need to tackle any document.

Common Questions About Indemnification Clauses

Even after getting the basics down, a few practical questions always seem to pop up. Let's tackle some of the most common ones.

Is an Indemnification Clause the Same as Insurance?

Not quite, but they’re related. Think of them as two different tools in your risk management toolbox.

An indemnification clause is a direct promise between two people in a contract. It's one person saying to the other, "If you lose money because of me, I'll cover it." Insurance, on the other hand, is a separate contract you buy from a third party—an insurance company—to pay for specific, covered losses. In fact, a contract might require you to have insurance to prove you have the cash to back up your indemnification promise.

The real difference is where the protection comes from. Indemnification is a promise from the other person in your deal, while insurance is a promise from a specialized financial company.

Can I Just Cross Out an Indemnification Clause I Don’t Like?

You could, but it’s almost never a good idea. Just striking out a clause without any discussion can make you look uncooperative, and the other party might just walk away from the deal. It's a pretty aggressive move.

A much better approach is to start a conversation. You can suggest specific edits that make the clause feel more balanced. For example, you could propose to:

- Make the clause mutual, so it protects both of you equally.

- Limit the scope to losses directly caused by your actions, not just anything that happens.

- Add a line clarifying that you aren't on the hook for their own mistakes.

Negotiating shows you’re taking the agreement seriously and are committed to finding a fair middle ground. That’s always more productive than just taking a red pen to the page.

What Happens If a Contract Doesn't Have an Indemnification Clause?

If a contract doesn't mention indemnification at all, any disputes over who pays for a loss will be handled under standard contract law. This usually means the person who lost money would have to sue the party they believe is at fault.

From there, they’d have to prove their case in court, which is a long, expensive, and unpredictable process. An indemnification clause helps everyone avoid that headache by setting the rules for responsibility upfront. It creates a much clearer and more direct path for sorting things out without immediately having to get lawyers and courts involved.

Trying to make sense of legal documents can feel overwhelming, but you don't have to figure it out alone. TermsEx uses AI to translate dense legal language into simple, easy-to-understand summaries. Just upload a document or paste a link to spot potential risks and unfair terms before you sign anything. Protect yourself by making smarter decisions. Check out TermsEx for free today.